September 2023 Commodities

Lumber futures gradually fall, metal markets “iron-ing” out new lows, and building material costs hold steady…

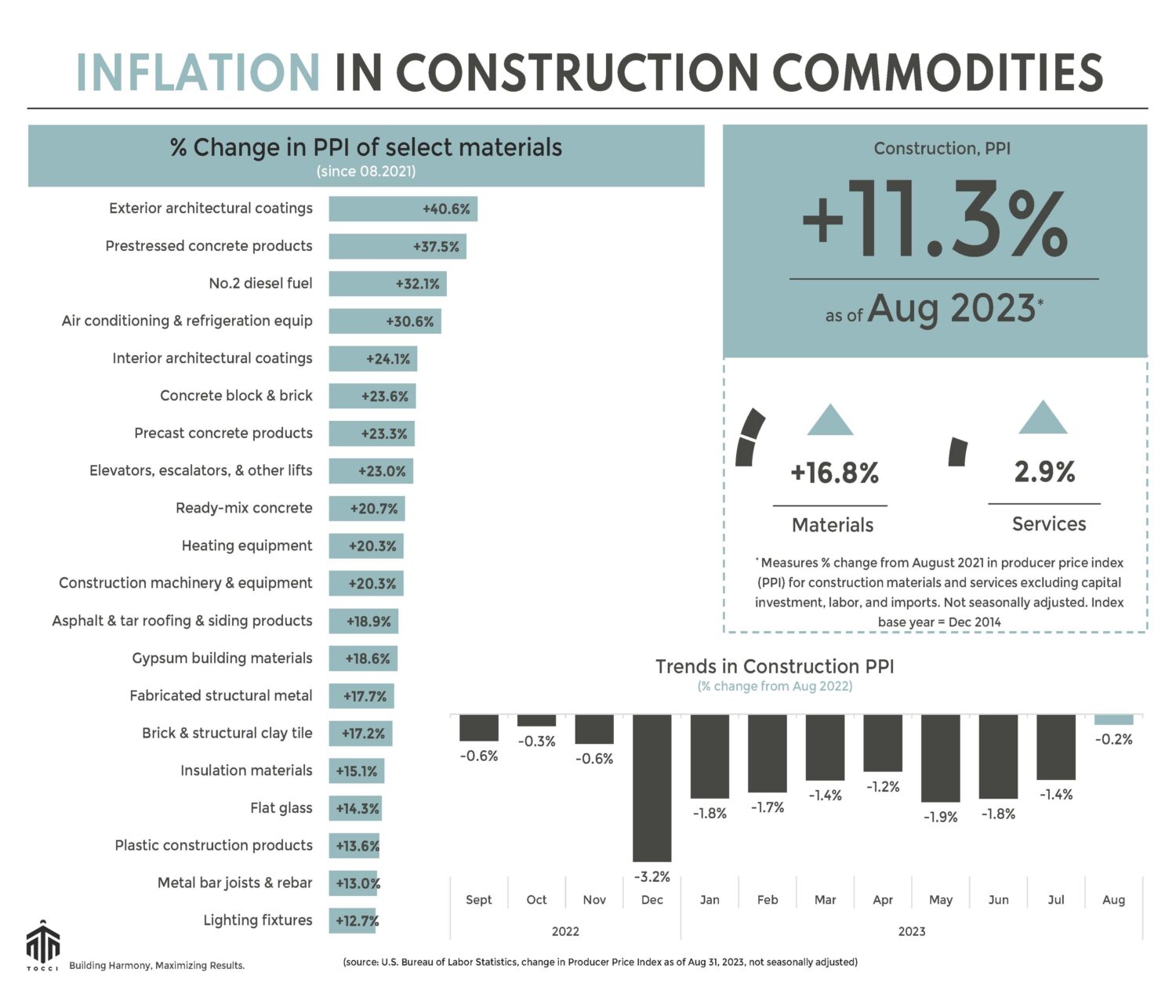

In August, the price level of construction inputs (materials and services) rose modestly compared to last month (+1.20%) but remained largely unchanged since last August (-0.23%).

Lumber: Lumber futures are taking a leafy plunge in September, mirroring the graceful descent of nature’s foliage; currently trading below $500/mbf (thousand board feet). It wasn’t too long ago that you needed a mortgage just to buy a 2×4, and that was if you were lucky to find inventory; it was a “log-istical” nightmare. But at least back then mortgage rates were seductively low. Today, the average 30-year rate is hovering above 7% and perched at levels last seen since the Y2K scare. Rising rates have led to a decline in homebuyer demand. Existing home sales are down 15.3%, year-over-year, according to National Association of Realtors. The weight of rising borrowing costs and muted homebuying is also impacting builder confidence for newly built single-family homes.

In September, the National Association of Home Builders (NAHB)/Wells Fargo Housing Market Index (HMI), a barometer of builder sentiment, dropped into negative territory for the first time in five months. August saw a significant downturn in housing starts. Last week’s New Residential Construction report published by the US Census Bureau, reveals that housing starts sank 11.3% in August compared to the previous month and are nearly 15% lower compared to the same period last year. On the other hand, permits, a leading indicator for future residential construction, experienced a robust 6.9% month-over-month increase. This upswing was primarily driven by 14.8% surge in permits for multi-family housing, whereas permits for single-family housing saw a more modest rise of 2.0%. Every cloud has a sawdust lining. Currently, a sluggish housing market is giving supply chains a chance to catch their breath and regain a measure of stability. In August, Producer Price Index (PPI) for softwood lumber “saw-ftened” compared to the previous month (-4.4%) and dropped 18% from last year.

When tight capital markets are squeezing investment return thresholds and tightening the noose around development budgets, hard costs become a fragile subject. Earlier in the year, we launched a program aimed at helping developers find a path to pencil and build in harmony. Feel free to schedule a meeting with our team to learn how Project Rescue is hammering out strategies and solutions.

STEEL and others: Hot-rolled coil (HRC) futures are sinking to levels last seen since October 2022. As September draws to a close, HRC futures linger close to $700 per short ton (st). This marks a 41% decline from their peak in March when HRC futures were trading in four-digit figures. HRC prices are bending under the weight of lackluster global demand, while casting wary glances at the growing specter of United Auto Workers’ strike at three major U.S. automakers. August’s Producer Price Index (PPI) for steel mill products exhibits a slight dip from the previous month (-0.5%) and remains steeped in deflationary undertones (-14.8% YoY.) Cold-rolled steel sheet and strip inched lower, -1.9% month-on-month, and plummeted -23.4% in comparison to last August.

While metal markets continue to face deflationary pressures, there are divergent trends in energy and fuel, nonmetallic mineral products, and construction equipment. No.2 diesel surged 34.6% in August compared to the previous month. The month-on-month PPI changes in nonmetallic mineral products remained generally stable. However, when compared to the previous year, cement is up 11%, ready-mix concrete +9.6%, gravel and crushed stone have risen by 8.2%, brick and structural clay have increased by 6.4%. Construction machinery and equipment +6%, and elevators and other lifts have risen by 5.9%.

Amidst the hurdles and headwinds in the construction world, we remain steadfast in our mission. Every challenge we face is an opportunity to innovate and drive value. Stay steady on the foundation. Together, we can Optimize Construction and Change the Industry!

See below for a commodities snapshot, or click here for the full report.