April 2024 Commodities

Lumber futures tumble, metals ebb and flow, and construction costs scale up

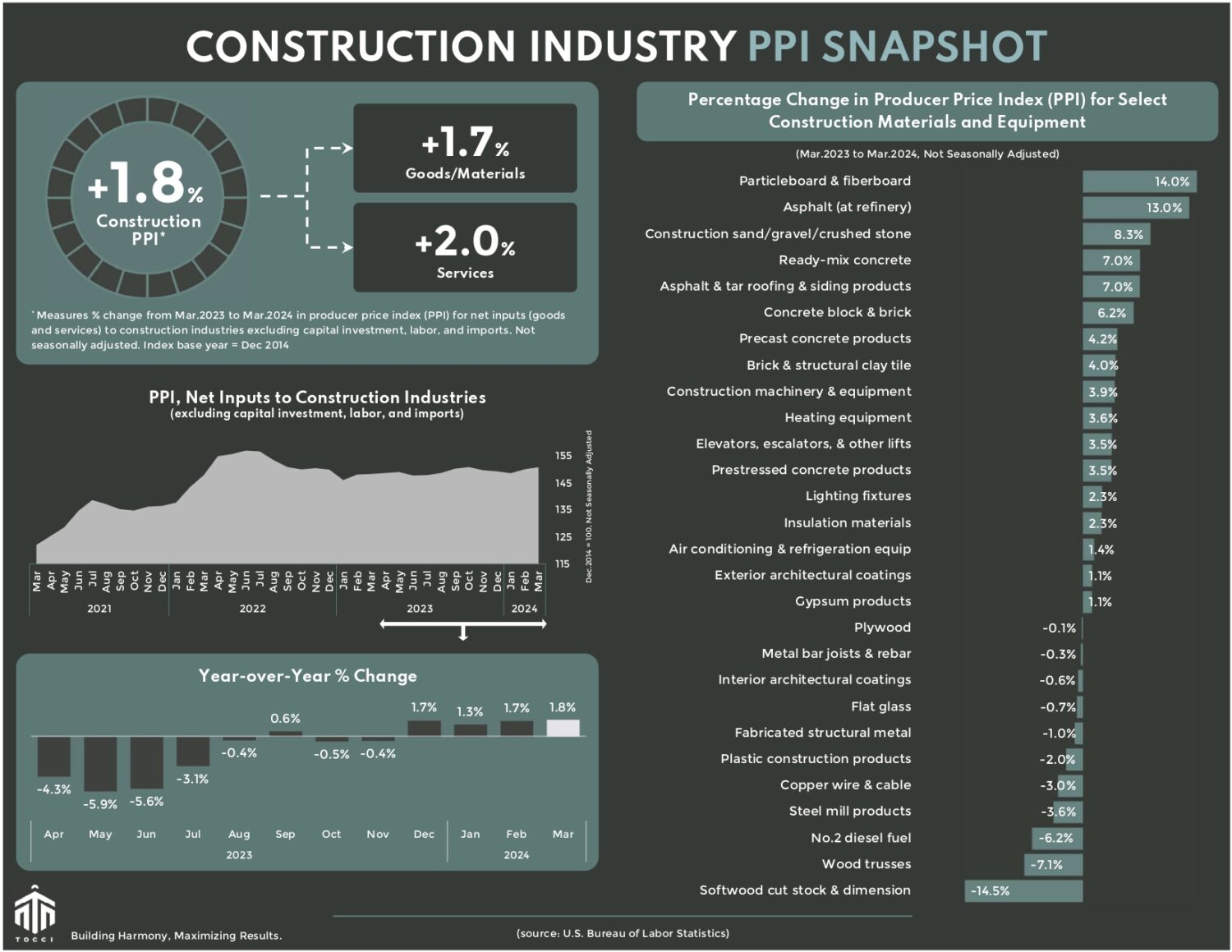

Construction costs continue to scale up. In March, the Producer Price Index (PPI) for construction inputs, a broad measure of inflation in materials and services for construction, rose by 0.4% compared to the preceding month and marked a 1.8% increase from a year ago.

LUMBER: As April unfolded, lumber futures took a tumble, falling nearly 15% over the past month to settle around the low $500s per thousand board feet. This indicates a palpable slowdown in the housing construction sector, signaling a waning appetite for softwood lumber products.

Digging into the numbers, the PPI for softwood lumber showed a 6.8% decrease in March, compared to a year ago despite ticking up 3.2% month-over-month. The NAHB/Wells Fargo Housing Market Index (HMI), a barometer of homebuilder sentiment, remained steadfast at 51 in April, indicating no change from March. However, data from new residential construction activity indicates a dip in momentum. After a surge in February, residential construction starts nosedived in March, wiping out all gains since the start of the year. The latest report from the U.S. Census Bureau, reveal a glaring 14.7% plunge compared to February, with an additional 4.3% retreat from the same period last year. The decline was particularly pronounced in multifamily housing, which saw a staggering drop of 20.8%, while single-family housing wasn’t spared, experiencing a decline of 12.4%.

Meanwhile, on the financial front, bond yields gain ground as consumer inflation rebounds, deflating hopes of a near-term interest rate cut. The average 30-year mortgage rate recently inched up to 7.24% from 7.13%, according to the Mortgage Bankers Association. Rising interest rates cast a shadow over housing construction activity, dampening demand for lumber and suppressing price growth.

STEEL and others: In late March and early April, U.S. hot-rolled coil (HRC) futures saw dramatic swings in the wake of the Francis Scott Key Bridge collapse and the temporary closure of the Port of Baltimore. Trader speculation sent HRC futures soaring 20% in a day. However, news of the port’s partial reopening at the end of April dissipated concerns of lingering supply chain disruptions. HRC futures swiftly retraced their meteoric rise back to the low $800s per short ton.

Amidst the ebb and flow of futures, the PPI for steel mill products broke a three-month streak of gains, sinking by 7.8% in March compared to the previous month and sagging 3.6% compared to the previous year. Beyond steel, gypsum products bounced up again this month with a 1.9% increase in March (month-over-month), while the PPI for asphalt (at refinery) spiked 11.2% compared to the previous month. No. 2 diesel posted almost no change from the previous month but increased by 11.4% since the start of the year. Moreover, in the past three months or year-to-date, noteworthy increases have been observed in ready-mix concrete (+3.3%), brick and structural clay tile (+3.6%), insulation materials (+4.1%), gypsum products (+4.4%), as well as hot-rolled steel (+3.9%).

From laying the foundation of accurate construction cost estimations to erecting a fortress of value engineering, we’re here to scaffold your project. Let’s connect and cement some ideas together.

See below for a commodities snapshot, or click here for the full report.