March 2024 Commodities

Lumber futures gain ground, metals PPI firm up, and construction materials continue to rise …

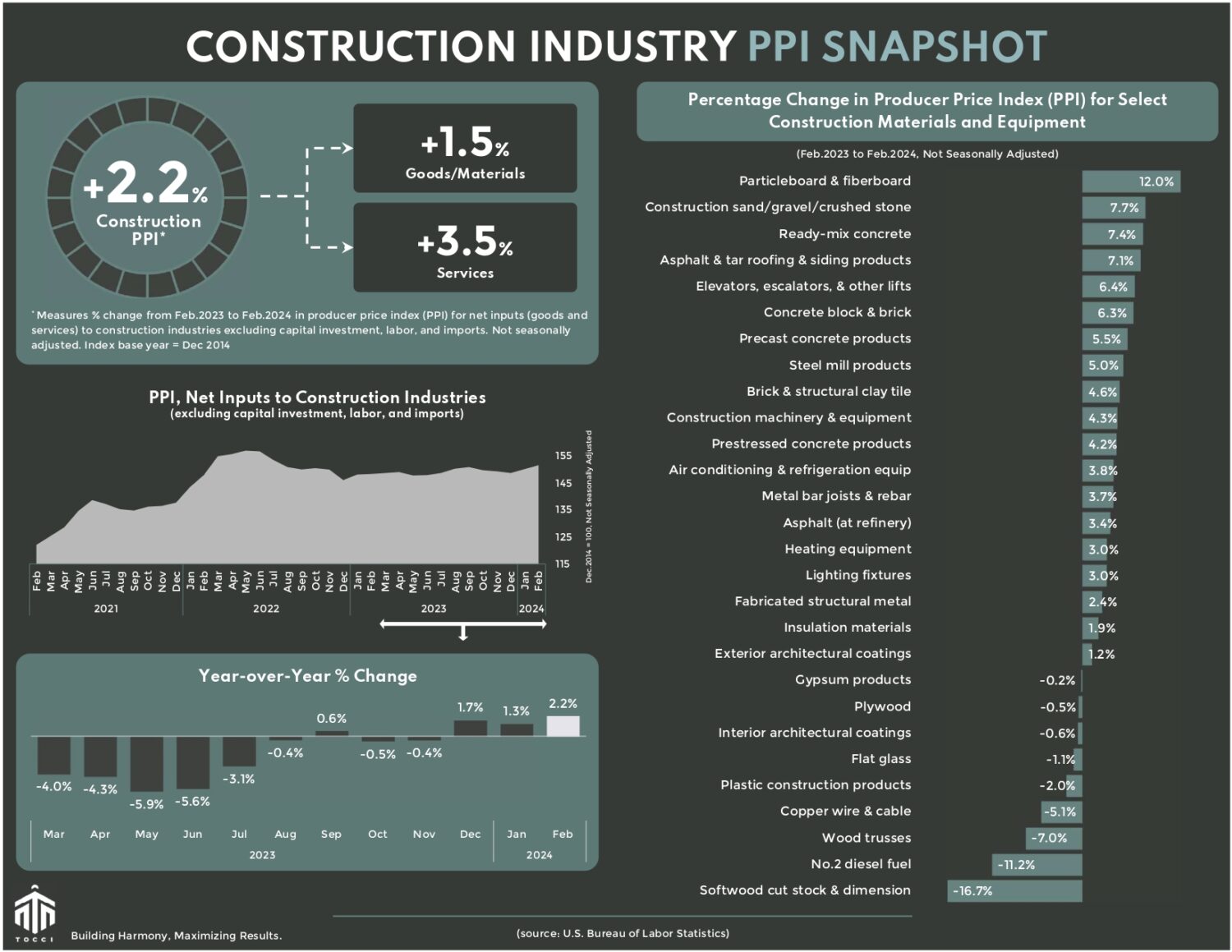

Construction material costs are on the rise again. Overall, the Producer Price Index (PPI) for construction inputs, a broad measure of inflation in materials and services for construction, rose in February by 1.0% compared to the previous month, marking a 2.2% increase from the same period last year. And that’s not all – the index is also the highest it’s been since August 2022.

LUMBER: Softwood lumber prices have been trending higher since last October. Lumber prices gained ground throughout March, with futures climbing above $600 per thousand board feet (mbf) for the first time in over a year, reaching a 52-week high of $624/mbf on March 12. The resilience in price growth was further underscored by the PPI for softwood lumber, which notched its third consecutive monthly increase in February, surging by 1.7% compared to the prior month and recording a 3.2% rise over the past three months.

Homebuilder optimism soared as well hitting an eight-month high, according to the National Association of Home Builders/Wells Fargo Housing Market Index (HMI). After rising for a fourth consecutive month, homebuilder sentiment scaled up to 51 in March. Readings that exceed 50 indicate positive market sentiment and industry outlook. US Census Bureau’s February report posted significant growth in new residential construction with housing starts increasing by 10.7% compared to the previous month and 5.9% compared to the previous year. Single-family housing starts led the charge, leaping by double digits both month-over-month and year-over-year; 11.6% and 35.2%, respectively. Construction permits, a barometer for future building activity, also showed promise, particularly for single-family units, which saw a substantial 29.5% increase year-over-year.

Looking ahead, expectations for rate cuts remain on the horizon and as interest rates stabilize, residential construction activity is poised for growth. The trajectory of interest rates holds significant sway over the future landscape of homebuilding, casting ripples through lumber markets.

STEEL and others: PPI for steel mill products rose for a third consecutive month maintaining its momentum with a 2.9% leap in February compared to the previous month and outpacing the previous year by 5.0%. Beyond steel, other materials have also experienced shifts worth noting. Gypsum products, after a prolonged decline, saw a 2.5% increase in February (month-over-month), breaking a ten-month streak. Similarly, PPI for insulation materials cozied up to a modest 2.1% increase compared to the previous month. Amidst these fluctuations, no. 2 diesel rages with a startling 18.3% surge in just a month, though still trailing behind last year’s pace by 11.2%.

Moreover, in the past two months (year-to-date), significant increases have been observed in cold rolled steel sheet and strip (+9.7%), cement (+4.0%), steel pipe and tube (+3.5%), gravel and crushed stone (+5.2%), ready-mix concrete (+2.8%), and brick and structural clay tile (+3.4%).

As we navigate through these fluctuations, let’s remain vigilant, observing the subtle shifts that shape our industry’s landscape. Together, let’s stay informed and prepared for whatever twists and turns lie ahead.

See below for a commodities snapshot, or click here for the full report.