October 2023 Commodities

Lumber futures tumble, steel futures heat up, and building material prices inch higher …

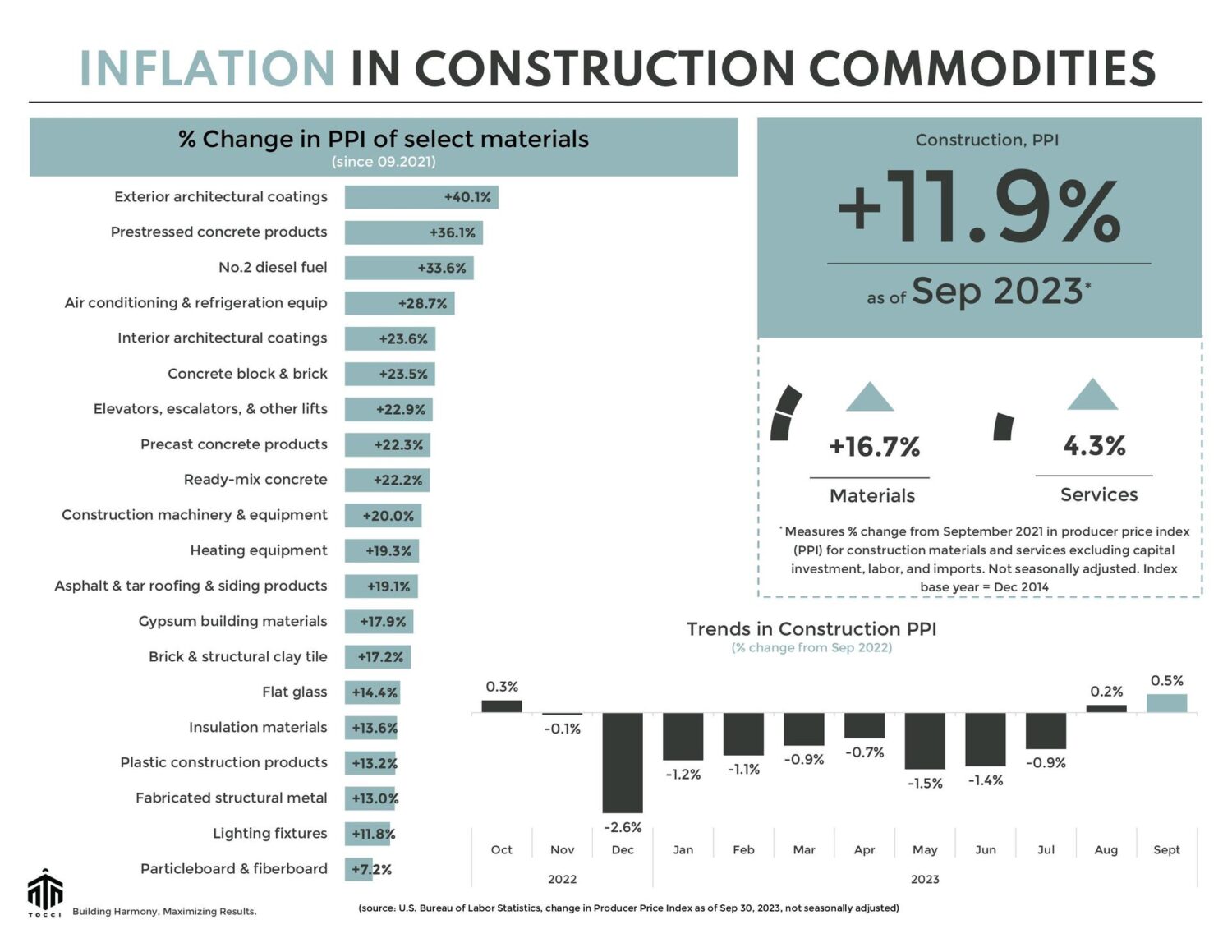

In September, the Producer Price Index (PPI) for construction inputs (materials and services) showed a slight increase of +0.29% compared to the previous month and a year-over-year rise of 0.48%.

Lumber: Futures continue to drop in October; currently trading below $495 per thousand board feet (mbf). This marks a notable 5% drop from the previous month and a substantial 20% decline from the same period last year. Prices of US softwood lumber prices have been on a downward trajectory since mid-2022. The precipitous fall can be attributed to a wane in demand after prices reached historic highs in the spring of 2021, coupled with the dissipation of supply-side disruptions as mills normalize their operations and output. The Producer Price Index (PPI) for softwood lumber sheds light on this trend, revealing a month-on-month decrease of -1.7% in September and a more significant 15.2% decline compared to the previous year.

Recent data from the US Census Bureau regarding new residential construction paints a cautious picture. Permits, a vital indicator of future construction activity, saw a 4.4% decline in September month-on-month and a 7.2% drop year-on-year, on a seasonally adjusted basis. Housing starts, although up by 7.0% compared to the previous month, remained 7.2% lower than the same period last year.

Adding to the complexity, 30-year fixed mortgage rates in October reached a 20-year high at 8%, significantly dampening builder sentiment. The National Association of Home Builders (NAHB)/Wells Fargo Housing Market Index (HMI), a key measure of builder confidence, dropped four points in October, marking the third consecutive monthly decline.

Securing funding for projects is growing more difficult because capital markets are demanding higher premiums on risk adjusted returns due to elevated borrowing costs and rising bond yields. Builders are adapting to tight market conditions via strategies aimed at softening hard costs and accelerating project delivery. But effective strategies often hinge on not just what we do but more critically when we do it.

Ask us how we execute Project Rescue.

STEEL and others: Like a tightly coiled spring suddenly set free, hot rolled coil (HRC) futures recently bounced back. Towards the tail end of October 2023, HRC futures didn’t just rise; they suddenly soared, smashing past $800 per short ton (st). In the 30 days leading to October 25, 2023, HRC futures experienced an 18% surge. US steel mills have once again flexed their pricing muscles. On October 19, Nucor and Cleveland-Cliffs cranked up the minimum rates for HRC, pushing the needle to $800/st. Just this week, we received word from a local structural steel fabricator that prices are creeping back up.

However, these price hikes are yet to make their mark on government data. In September, the Producer Price Index (PPI) for steel mill products took a little dip, with a 3.7% decline compared to the previous month and recorded a 12.1% retracement year-on-year. Yet, it seems only logical to anticipate a rise in PPI for ferrous commodities in the upcoming months.

Meanwhile, PPI for nonmetallic mineral products remained steady, except for concrete pipe, which leaped 9.4% in September compared to the previous month. No.2 diesel fuel, the kind you find at gas stations, increased by 4.3% month-on-month. Still standing tall from the previous year are concrete pipe (+16%), cement (+10.8%), gravel and crushed stone (+8.5%), and construction machinery and equipment (+6.1%).

Sudden and stealthy material price fluctuations can jeopardize project budgets. But when engaged early in design, a collaborative construction manager can deliver cost effective alternatives while preserving original design intent.

See below for a commodities snapshot, or click here for the full report.