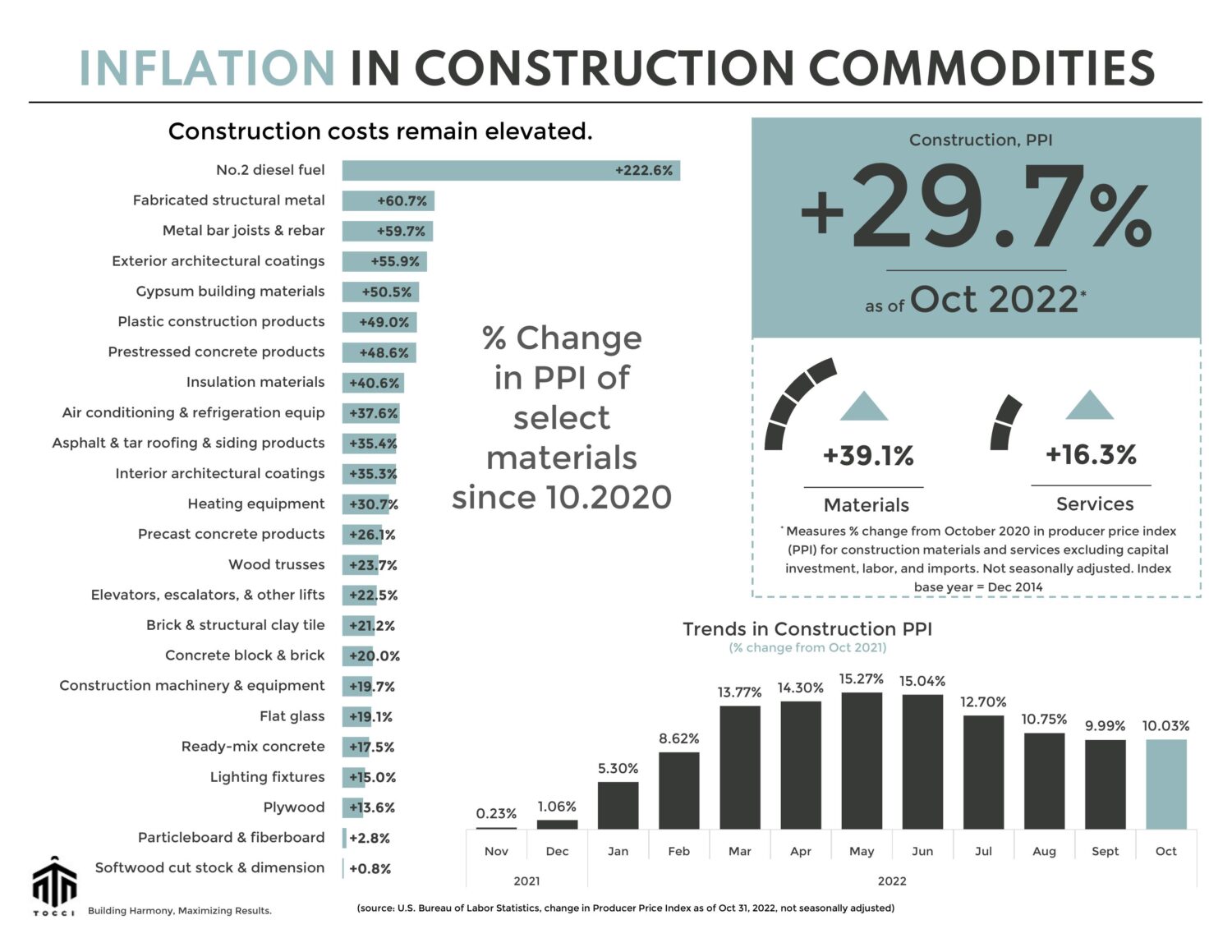

November 2022 Commodities

Lumber futures slip, metal markets rust, and construction inflation creeps up…

LUMBER

All’s quiet on the housing front… and the silence is dulling lumber prices. Muted demand in the housing market catalyzes further downward price pressure in wood products. Despite the mini lumber rally in October, BLS’s latest PPI print registered another month-on-month drop in Softwood Lumber -1.8%, Plywood -1.4%, and Hardwood Lumber -5.4%.

In November, lumber futures sold off into the mid-$400 per thousand board feet (mbf) and seem to have found a bottom at around $420/mbf. For perspective, prices were gaining momentum this time last year and by the end of 2021 were trading above $1,000/mbf. Although it’s unlikely lumber will skyrocket back to quadruple digits, a bump in prices is expected (seasonal buying). Market volatility? Less dramatic than last year. A much-needed reprieve for estimating teams.

STEEL and others

Ferrous commodities sold off aggressively since the beginning of the year and prices continue to dampen across a broad range of metals and metal products. Hot-rolled coil (HRC Steel) futures recorded a new 52 week low in November, reaching $657/short ton (st); amounting to a 60% drop from a year ago. PPI for Steel Mill Products slid 6.6% in October compared to the previous month.

The sharpest monthly drop was in Cold Rolled Steel Sheet and Strip (-16.5%) followed by Stainless Steel Scrap (-8.4%) and Aluminum Scrap (-7.4%). What’s depressing prices?

- A weak U.S. export market;

- high supplier inventory levels; and

- lethargic manufacturing activity.

Outside the forest and furnace, inflation moderates. Great! But we’re out of the frying pan and into the fire – capital markets are getting tighter. Reach out to TOCCI to find out how we can help you value engineer your budgets. Ask us how Target Value Design works.

See below for a commodities snapshot, or click here for the full report.