October 2022 Commodities

Lumber futures tick up, steel prices cool off, and construction inflation edges lower…

LUMBER

September’s PPI print recorded another month-on-month drop in a broad range of wood products; Softwood lumber -4.6%, Plywood -1.2%, and Hardwood lumber -6.0%. However, lumber futures gained momentum during the 2nd half of October and are trading above $500/mbf; a modest +22% increase from last month, as of October 24. Why?

1. Cyclical buying kicks off in the winter as builders ramp up orders ahead of next year’s building season.

2. Lumber producers are reducing output in a bid to buoy prices.

Interfor, Canada’s largest lumber producer, announced yesterday they plan on chopping their production by 17%! Canfor and West Fraser (other Canadian lumber behemoths) also announced production curtailments. Not good. This signals to market participants that the hiatus of bargain lumber prices ends here. Another factor that could apply upward pressure on lumber prices is the unassessed damage along the southern Atlantic coast caused by Hurricane Ian, that could spur a flurry of rebuilding and prop up demand for wood products.

Yet, while the housing market remains depressed under the crushing weight of hawkish monetary policy, we can expect lumber prices to remain tame. Of course, that can change in a heartbeat if the Fed turns the money spigot back on. If we’re certain of uncertainty, would the best course of action be inaction? Not necessarily – that’s how opportunities are lost. Reach out to TOCCI so we can explore them together through our Design Phase Management program.

STEEL and others

PPI for Steel Mill Products registered negative growth in September compared to a month ago and is down nearly -15% compared to the previous quarter. A broad range of ferrous products slid in September and are down double digits compared to last year. Yet, PPI for steel mill products is up +91% since Feb 2020 (pre-COVID). Hot-rolled coil (HRC Steel) futures recorded a new 52 week low in October, reaching $680/short ton (st). Softened demand for industrial metals and high energy costs are driving steelmakers to lower output. U.S. Steel recently idled two blast furnaces that have a combined annual capacity of 2.9 million st.

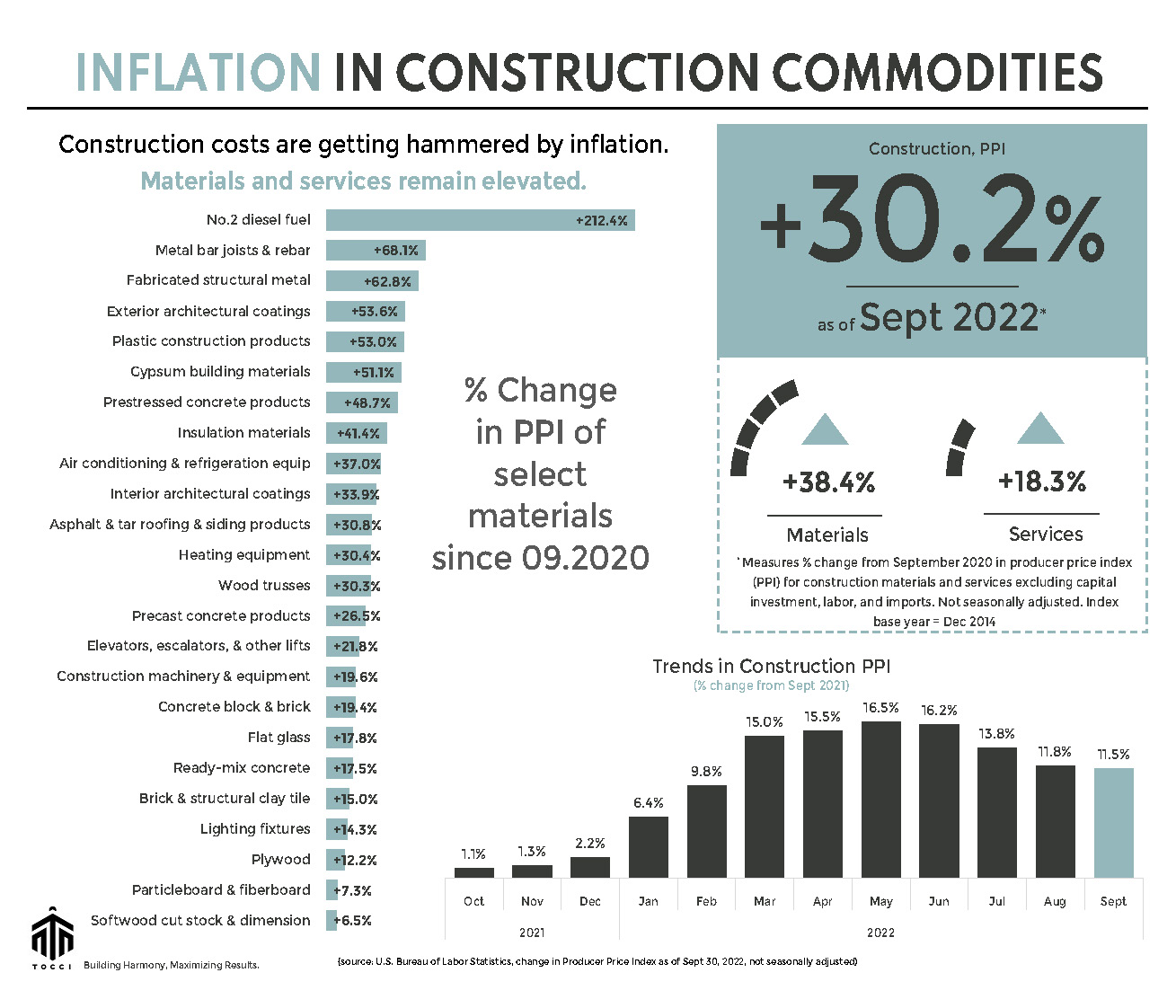

Outside the forest and furnace, inflation in construction commodities persists. Year-to-date, Gypsum products are up +16.2%, Plastic pipe, fittings and unions +16.8%, Asphalt +42.2%, No.2 diesel +60.1%, Prestressed concrete products +30.5%, Air conditioning and refrigeration equipment +17.3%, and Insulation material +13.3%. Price volatility induces shortages and questionable material availability that will impact project delivery.

A seasoned CM can help you navigate alternatives to delicately optimize materials and system selection. Feel free to ask us how.

See below for a commodities snapshot, or click here for the full report.