May 2023 Commodities

Lumber markets embrace new futures contract, steel prices are gliding down, and construction inflation inches higher…

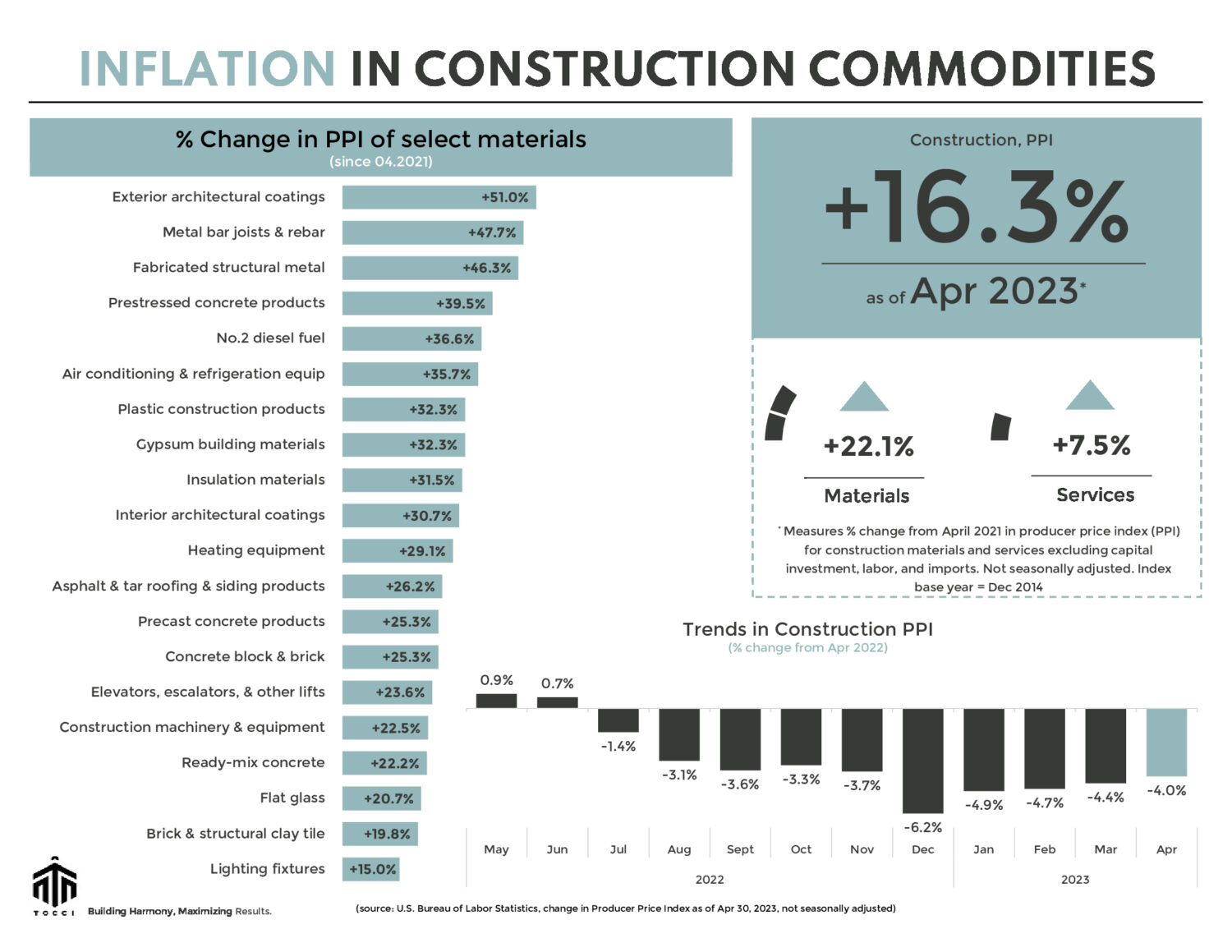

Construction input prices moderated for a second consecutive month in April. PPI for construction materials and services sees marginal monthly increase (+0.43%), while YoY decline persists (-4%).

LUMBER

In May, we bid farewell to the lumber futures contract that surged during the pandemic and reached a record high of +$1,700 per thousand board feet. The lumber futures contract (Random Length Lumber), known for its price surge and volatility during COVID-19, concluded its final trading session on Monday, May 15, 2023. To replace it, CME Group (Chicago Mercantile Exchange) debuted a new lumber futures contract, Lumber (LBR), and began a gradual phase-out of the old contract last year. Designed to align with the approximate quantity of lumber required to construct a house, the new futures contract brings heightened risk management capabilities for builders and mills. Moreover, its enhanced features aim to entice a broader range of market participants to actively engage in lumber futures trading and boost market liquidity and price stability.

April’s New Residential Construction print showed mixed performance. Single-family construction starts grew modestly by 1.6% while multifamily construction starts saw a stronger increase of 5.2% compared to the previous month. Home builders’ confidence rose for a 5th consecutive month since December but despite the growth, single-family housing starts remained lower than the previous year (-28.1%), indicating ongoing market challenges.

Double-digit price hikes and long lead times persist for certain construction materials while financing costs remain high. However, amidst these challenges, we have developed Project Rescue to address your concerns and unpack opportunities. Feel free to ask us about it.

STEEL and others

Steel markets seem to be losing momentum after experiencing a robust rally since last December. In May, Hot-rolled Coil steel futures retraced below $1,000 per short ton and are down nearly 14% compared to last month. After months of price hikes, mills are now vying for market share and accepting lower offers amidst a slowdown in buying behavior. April’s Producer Price Index (PPI) data shows mixed trends in pricing for non-ferrous construction commodities compared to the previous month. Asphalt prices surged by 15.3%, while No.2 diesel fuel witnessed a decrease of 5.2%. Concrete block and brick prices saw a slight increase of 1.3%, along with ready-mix concrete, which rose by 1.0%. Although flat glass tempered month-on-month, it still remains 9.3% higher than the previous year.

In a landscape of constantly changing costs, project budgets can easily be disrupted, and timetables derailed. Transparent collaboration between owners, architects, and builders during pre-development is required to identify potential roadblocks and proactively address them. Discover how our Design Phase Management services are empowering owners to effectively hedge against project delivery challenges. Reach out to learn more about our streamlined approach.

See below for a commodities snapshot, or click here for the full report.