June 2023 Commodities

Lumber futures gain momentum, steel prices retrace, and construction inflation sags…

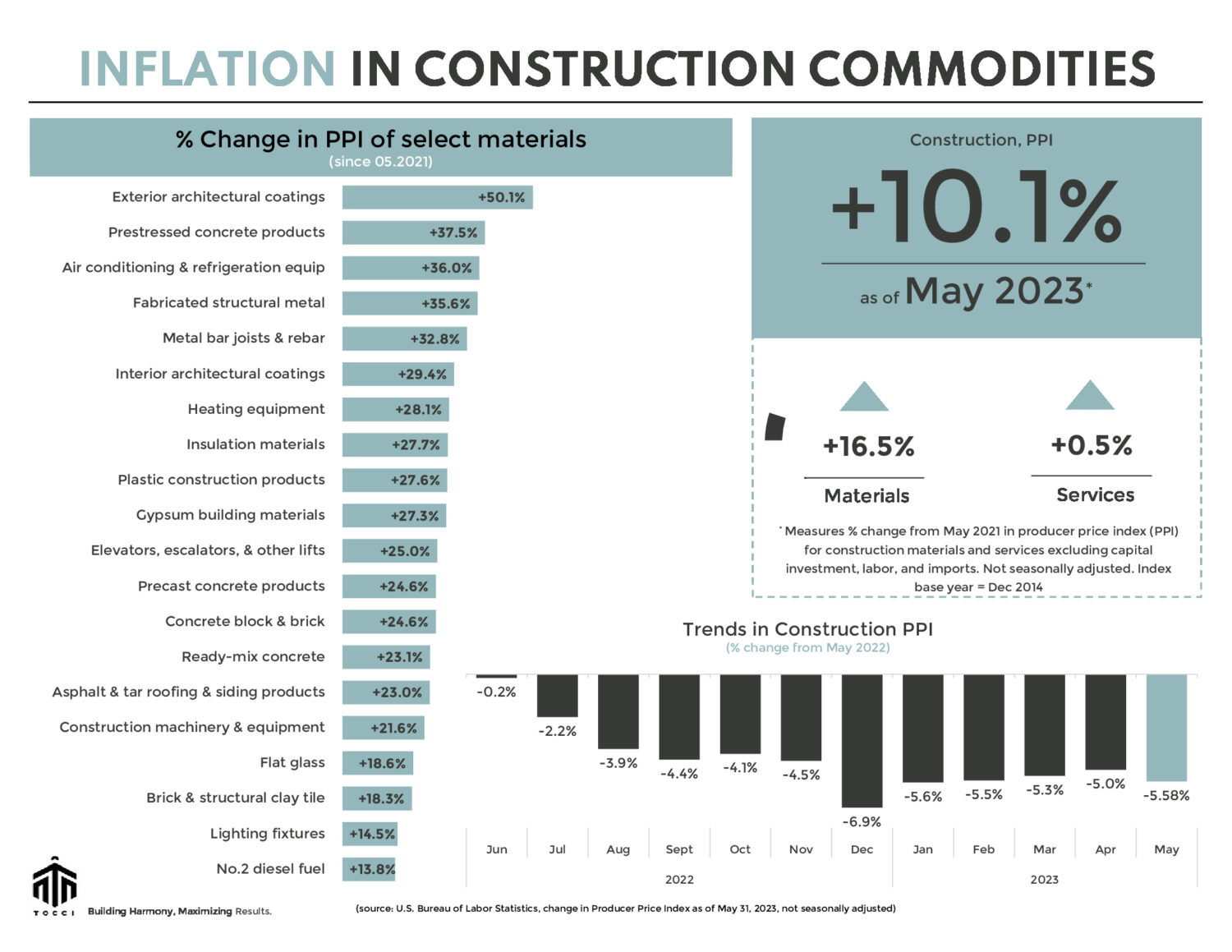

Construction input prices glide lower in May with the Producer Price Index (PPI) for materials and services falling by -0.64% from April and -5.58% from last year.

LUMBER

Last month, the Chicago Mercantile Exchange (CME Group) retired the old lumber futures contract and phased in a more compact version designed to enhance trading liquidity and price stability. Lumber futures have been climbing steadily, increasing by nearly 16% since June 1st, and currently trading around $550 per thousand board feet (mbf). However, there’s no smoke without fire (literally). Forest fires have been mercilessly blazing throughout Alberta and British Columbia causing production disruptions. These wildfires have influenced lumber prices, as mills are forced to halt operations. The French have a fancy term for this, force majeure.

Another factor contributing to rising wood prices is activity in the homebuilding sector. May’s new residential construction report reveals a remarkable month-on-month surge in starts (+21.7%) coupled with a healthy increase in construction permits compared to last month (+5.2%). A renaissance in demand from first-time homebuyers amidst a shortage of existing housing inventory and healing supply chains is boosting homebuilder confidence. In June and for the first time in over a year, the NAHB/Wells Fargo Housing Market Index – a monthly survey measuring homebuilder sentiment – entered positive territory, indicating the potential for a rebound in homebuilding activity.

In commercial real estate, soaring financing costs plus a heightened focus on sustainability are highlighting engineered mass timber as a viable alternative to traditional structural systems that use carbon-intensive materials such as concrete and steel. The lumber market is experiencing dynamic changes and promising prospects. Reach out to learn how prefabricated wood can restructure your hard costs and construction schedule.

STEEL and others

Steel markets are facing major headwinds from anemic activity in the domestic manufacturing sector. In June, hot-rolled coil (HRC) steel futures traded flat within the mid to low $900s per short ton (st) range. Overall, steel futures are down nearly 18% in the past three months. Despite softening demand, several U.S. steelmakers defied the trend and announced price increases earlier this month. Nucor established a minimum HRC spot price of $900/st, while ArcelorMittal and Cleveland-Cliffs raised their minimum HRC spot prices to $950/st.

The PPI report in May revealed mixed pricing trends for non-ferrous construction commodities compared to the previous month. Asphalt prices increased by +9.0%, while No.2 diesel fuel experienced a decrease of -6.2%. Ready-mix concrete prices rose by +1.1%, whereas flat glass prices softened by -1.1%. As construction commodity prices ease, the industry is grappling with a steady rise in construction labor costs. The index for total compensation for private industry workers in construction increased by +4.9% in May compared to the previous year. Inflation in labor costs can be attributed to several factors, including a shortage of skilled tradespeople, competition from other industries, and a lack of interest from younger generations. As the industry’s workforce ages, the need to entice more workers will likely lead to higher wages. Don’t let labor-related constraints hinder your progress. If your budget is feeling the strain, we’re here to help.

See below for a commodities snapshot, or click here for the full report.