July 2023 Commodities

Lumber futures lose steam, metal markets turn fragile, and construction inflation flatlines…

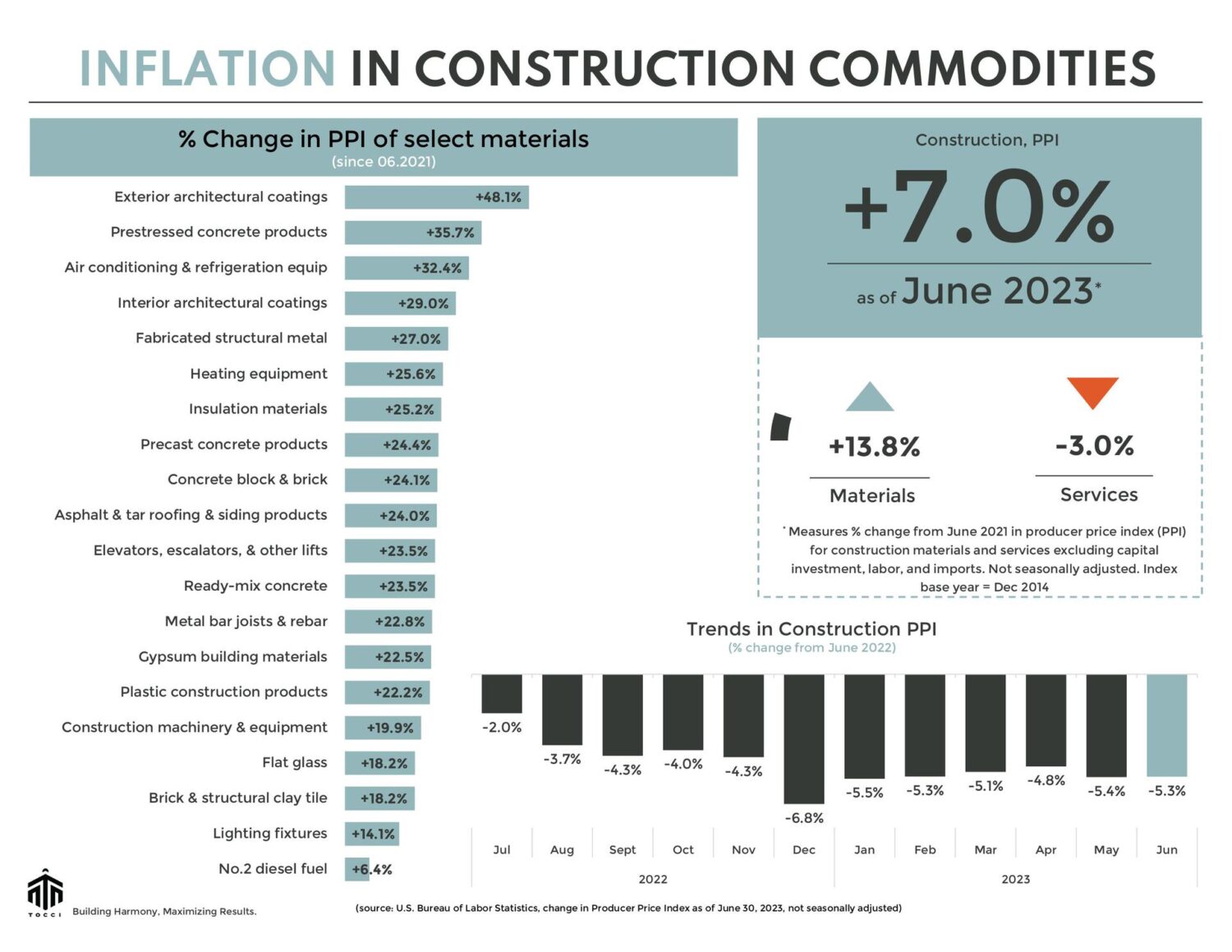

In June, the Producer Price Index (PPI) for construction inputs (including materials and services) registered insignificant monthly gains, with a shy uptick of +0.02%. However, compared to last June, a trend emerges, with a year-on-year decline of -5.34%.

LUMBER

Canadian forest fires last month had a scorching impact on lumber markets, causing prices to sizzle. Lumber futures soared, almost reaching $600 per thousand board feet (mbf) during the first half of July. Panic buying? Perhaps the threatened supply of softwood pine species rushed speculators to bid up the price of lumber futures. As Canada is the second-largest softwood lumber producer, any newsworthy disruptions raise worries about the availability and cost of this critical housing material. The hysteria was short lived, and futures retraced (now trading sub $525/mbf) when the New Residential Construction data for June was released. The data indicated suppressed growth in building permits and starts. US home building starts took an 8% dive in June compared to the previous month’s surge. And an 8.1% drop compared to the same period last year. Building permits weren’t spared either, taking a 3.7% hit compared to the previous month and a 15.3% decrease year-on-year. The landscape of higher interest rates, with the average 30-year fixed-rate mortgage gradually approaching 7%, adds to the cautious optimism among home builders.

The existing home market has turned into a desert with low inventory. Homeowners who scored low-interest loans (“forever mortgages”) during the Pandemic are holding on tight, reluctant to sell in a high interest rate regime. There’s a drought of existing homes available for sale, and that’s music to the ears of builders because buyers who haven’t been priced out are in the market for new construction. The NAHB/Wells Fargo Housing Market Index, a popular barometer for builder sentiment, has been consecutively rising for the past seven readings. Builder confidence is at its highest level in over a year! Fortunately, the cost and availability of lumber and wood products have improved. Compared to last year, PPI for softwood lumber is down nearly -21%, particleboard and fiberboard -23.4%, plywood -19.5%.

STEEL and others

In recent weeks, hot-rolled coil (HRC) futures market has seen a softening of prices, dropping by nearly 9.5% compared to a month ago (as of July 26). Currently trading below $850 per short ton (st), this decline is attributed to muted demand, a global supply glut and concerns about a potential recession in industrialized economies. Adding to the challenges, low import offers have put domestic steelmakers under competitive pressure. As a result, supply levels have improved, making it difficult for prices to maintain their previous highs. Domestic steelmakers are aware that significant price increases could drive buyers to foreign suppliers and imported steel bids. Compared to last June, PPI for steel mill products shrunk by 18%.

However, year-on-year inflationary trends persist in nonmetallic mineral (energy intensive) products such as cement (+13.3%), concrete pipe (+15.1%), ready-mix concrete (+12.1%), insulation materials (+7.7%) and flat glass (+8.5%). These price increases could lead to shaky foundations in your construction cost estimates. Our stellar Planning and Cost Engineering team boasts decades of experience and leverages an expansive database of material and labor pricing. A high-fidelity estimate can fiscally stabilize your investment thesis and reinforce your projections. Reach out if you want to refresh your pro forma with a robust construction budget.

See below for a commodities snapshot, or click here for the full report.