February 2024 Commodities

Lumber futures hold steady, metals PPI heat up, and construction inflation rebounds …

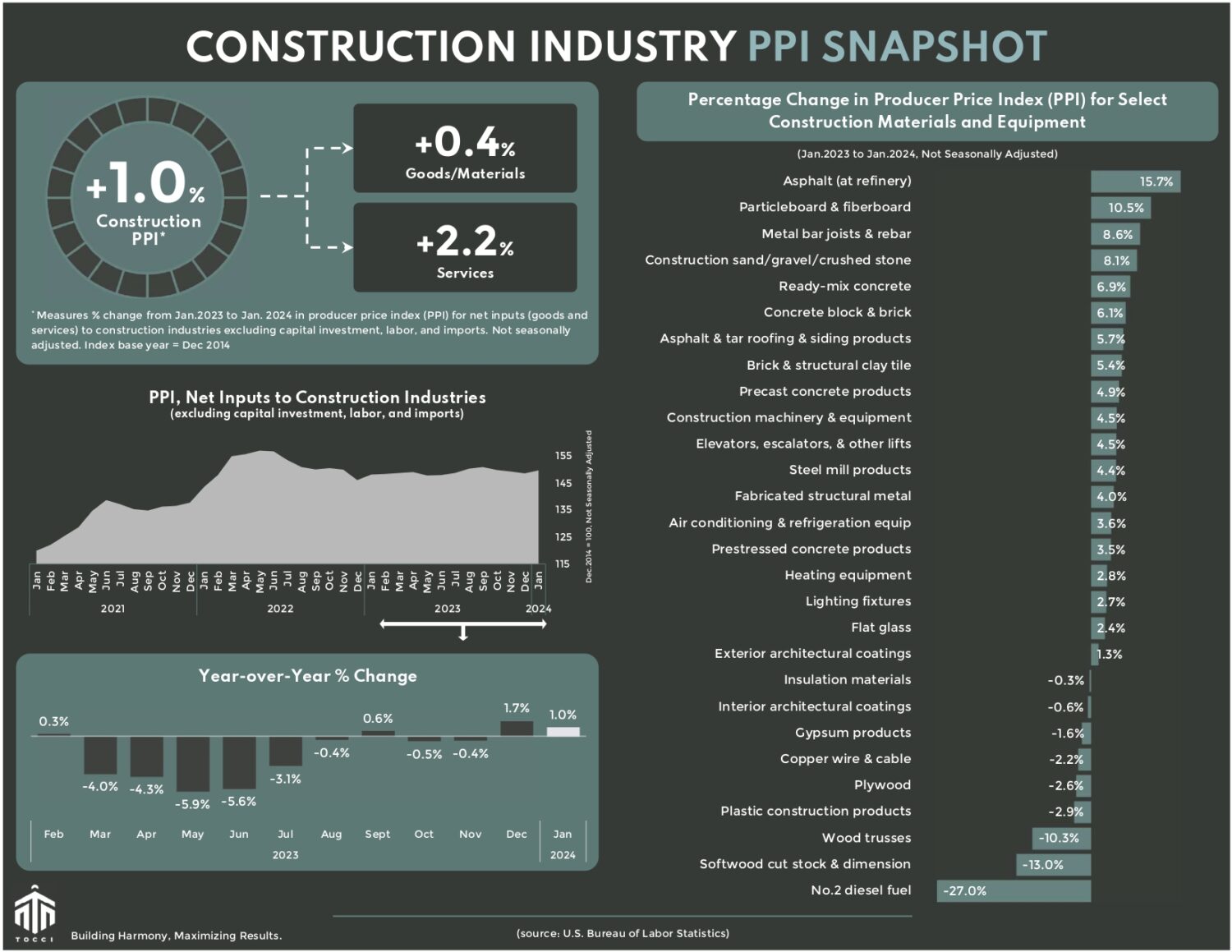

Overall, the Producer Price Index (PPI) for construction inputs, a broad measure of inflation in materials and services for construction, rebounded in January by 0.8% month-over-month after a quarter of declining growth and posted a 1% increase compared to the same period last year. While inflation may be striking a more moderate pose, construction costs remain elevated.

LUMBER: Steady and stable lumber prices in February, upheld by shy demand and ample supply, have seen lumber futures maintaining a steadfast level above $550 per thousand board feet. Despite the pervasive deflationary trend in lumber prices observed over the past year, signs of moderation are emerging, with the year-over-year decline narrowing to single-digit figures. January’s PPI for softwood lumber reported a 9% decrease compared to the same period the previous year.

The connection between homebuilding activity and the lumber market is influenced by homebuyer demand, a relationship susceptible to the sway of interest rates. Earlier this month, mortgage rates surged past 7%, driven by news of January’s inflation uptick, casting shadows over the prospect of a near-term rate cut. Consumer Price Index data, released earlier this month, came in higher than expected, sparking concerns about the possibility of the Federal Reserve keeping interest rates higher for longer.

As the curtain rose on 2024, the housing starts narrative unfolded with less-than-rosy news. According to the Census Bureau’s January report, housing starts took a 14.8% dip from December, showing a slight 0.7% year-over-year decrease (seasonally adjusted). In the single-family category, construction starts encountered a modest hiccup with a 4.7% decline for the month but remained firm with a 22% year-over-year increase. In contrast, multifamily starts (five or more units) underwent a substantial contraction, declining by 36% for the month and 38% year-over-year. Permits, an indicator of future construction activity, painted a mural of mixed emotions, displaying a 1.5% dip in January but sporting an 8.6% year-over-year increase primarily driven by a notable 35.7% surge in the single-family category. With rate cuts anticipated sometime this year, these figures underscore a bullish outlook for homebuilding and lumber demand potentially pushing prices beyond current levels.

STEEL and others: Breaking free from a streak of consecutive months with declining growth, PPI for steel mill products took a positive turn in December, sustaining its momentum into January with a notable 5.4% rise compared to the previous month. Year-over-year, PPI for steel mill products increased by 4.4%. Particularly striking is the PPI for cold rolled steel, which has surged by 35.5% compared to the same period last year. Other notable increases from a year ago include asphalt (at refinery) at +15.7%, cement at +8.2%, gravel and crushed stone at +8.1%, concrete product at +6.2%, and construction machinery and equipment at +4.5%. These sustained PPI growth trends indicate that prices for certain construction materials are likely to stay higher for longer.

See below for a commodities snapshot, or click here for the full report.