December 2023 Commodities

Lumber futures cozy up and steel futures rise, all while construction inflation is largely unchanged …

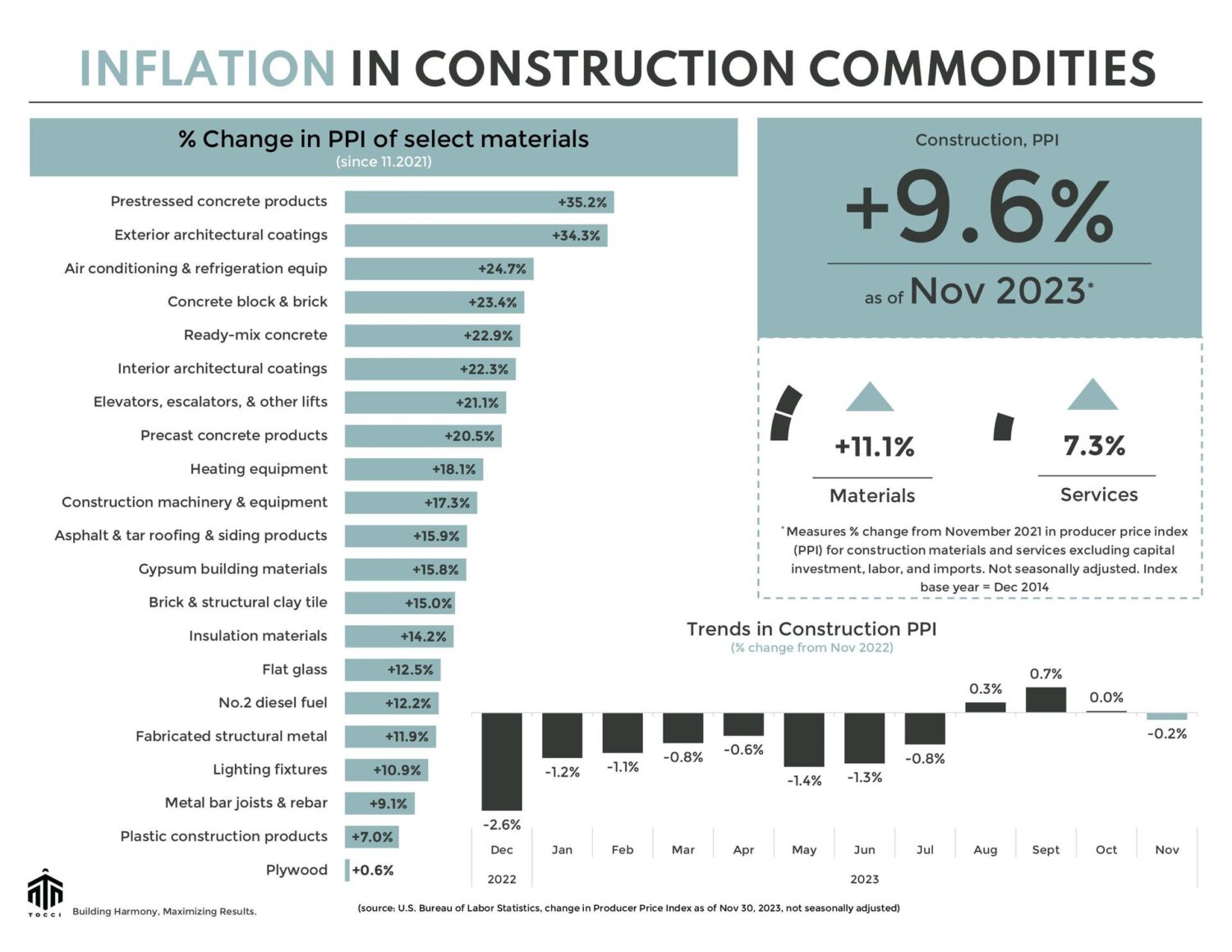

In November, the Producer Price Index (PPI) for construction inputs, a broad measure of inflation in materials and services for construction, experienced a marginal decrease of 0.23% from the previous month and a 0.18% decline compared to the same period last year.

LUMBER: As winter blankets us, lumber futures cozy up and found a snug spot above $525 per thousand board feet (mbf). Meanwhile, November’s PPI for softwood lumber registered a 5.1% month-on-month decrease and a 9.8% decline from the previous year on a non-seasonally adjusted basis. The index is now at its lowest level in the past three years.

On the financial front, mortgage rates dipped in the past month. The average 30-year fixed mortgage rate in December reached 6.83%, the lowest since June 2023, according to Mortgage Bankers Association. Notably, the US Federal Reserve maintained rates in December (for the third straight time) and indicated three rate cuts in the coming year. After reaching nearly 5% in October, yields on long-term US Treasury bonds started slipping from their recent peaks. In December, the yield on the 10-year U.S. Treasury dipped below 4%.

In the construction theater, housing starts took center stage in November, reaching their highest level since May. The Census Bureau’s New Residential Construction report revealed a 14.8% increase compared to the previous month and a 9.3% rise from the same period last year. Although building permits decreased by 2.5% on a seasonally adjusted basis compared to October, they still stand 4.1% higher than last year, signaling continued optimism for future construction activities.

The sentiment among U.S. homebuilders experienced a modest rebound in December, breaking a four-month decline. The National Association of Home Builders (NAHB)/Wells Fargo Housing Market Index (HMI), a barometer for single-family builder outlook, reported a three-point rise in builder confidence, reaching a level of 37.

STEEL and others: US steelmakers defy sluggish market with sticky price hikes. After effectively curating higher prices through a series of hikes in the past two months, U.S. flat rolled steel market maintains a bullish trajectory in December. Hot-rolled coil (HRC) futures have been heating up since October 2023, marking a nearly 10% increase over the last 30 days leading up to December 20, 2023. Currently, trading above $1,100 per short ton (st), HRC futures show a substantial year-on-year increase of 72.6%.

Despite this uptick in HRC futures, there is a contrasting trend in the PPI for steel mill products. November’s PPI for steel mill products reveals a 1.5% decline from the preceding month and an 8.4% drop year-on-year (not seasonally adjusted). The index for steel mill products has steadily decreased since June 2023, reaching its lowest level in the past two and a half years.

November’s PPI for nonmetallic mineral products (flat glass, cement, gypsum products, ready-mix concrete, etc.) remains largely unchanged month-over-month. However, prices in this category have firmed up in the past year; ready-mix concrete +9.4%, construction sand and gravel +8.4%, cement +8.3%, concrete pipe +7.1%, brick and structural clay +5.6%. Notable declines can be found in no.2 diesel fuel and plastic pipe where the indices dropped nearly 30% and 12%, respectively, compared to the same period last year.

The current trend of moderating construction costs, coupled with low volatility and softening interest rates, creates a favorable landscape for developers and builders. Let’s explore this opportunity and consider building something together.

See below for a commodities snapshot, or click here for the full report.