August 2023 Commodities

Lumber futures flaccid, metal markets lose steam, and construction inflation drops steadily…

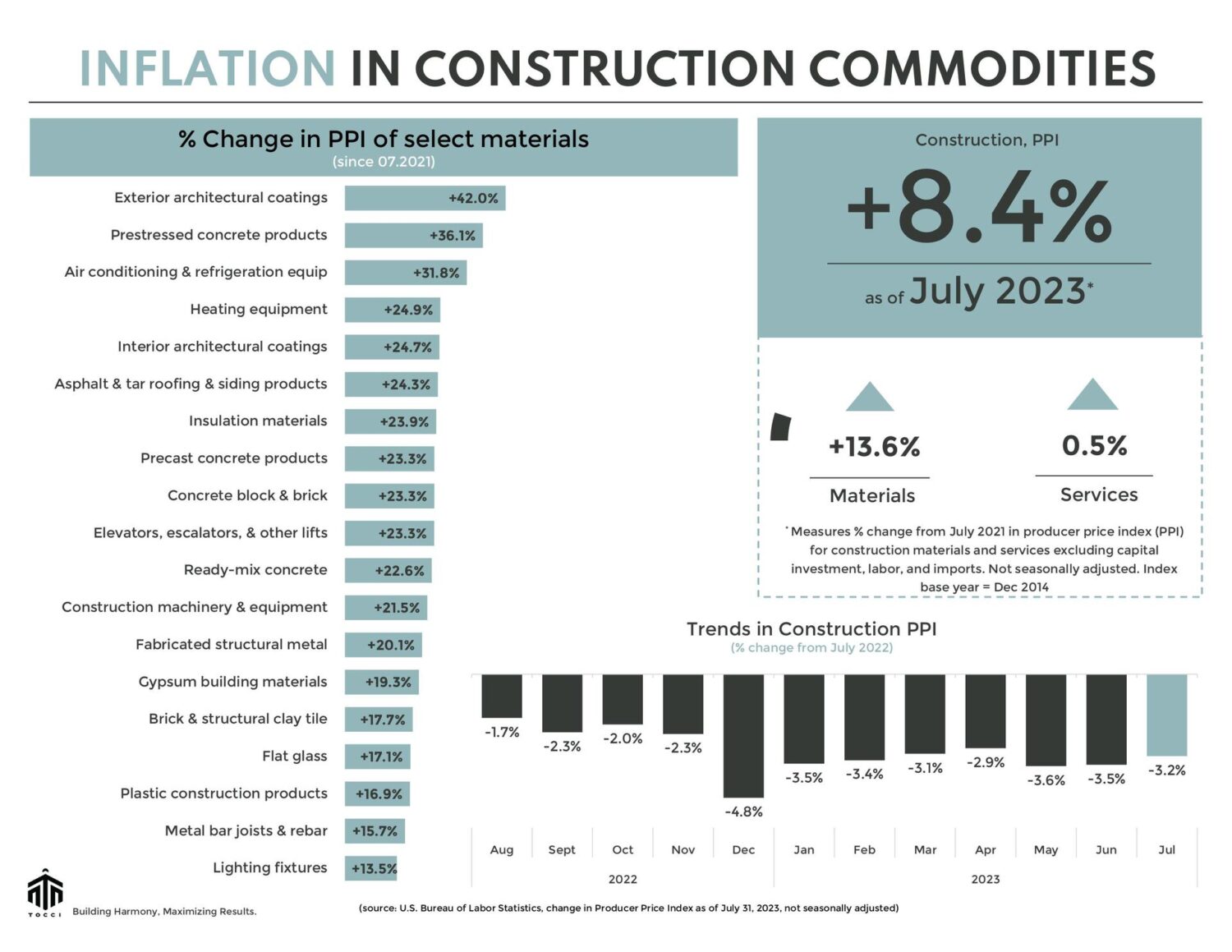

In July, the Producer Price Index (PPI) for construction inputs ( materials and services) shimmied up +0.35% compared to last month but dropped -3.20% since last year.

LUMBER

Throughout most of August, lumber futures seesawed within a tight range of $500/mbf to $525/mbf (thousand board feet). Gone are the days of lumber behaving like a caffeinated squirrel on a trampoline; the current scene resembles a Zen garden of tranquility. Supply chains that were strained in recent memory have regained a measure of stability and tempered buyer urgency. Another factor that’s giving the market a dose of equilibrium is the absence of speculative buying that rallied the price of lumber to over $1,700/mbf in May 2021.

Switching gears to July’s Producer Price Index (PPI), softwood lumber shifted up (+4.4%) compared to the previous month. But that uptick is overshadowed by a double-digit (-17.3%) plunge from the previous year. Venturing beyond the lumberjacks’ domain, the U.S. housing landscape is a scene of chaos and confusion. Average 30-year mortgage rates have tripled in the past two years. With rates flirtatiously close to 7.50% and sticky home prices (blame the housing shortage) we have a formidable tag team, effectively giving a championship belt to unaffordability. Into the latest New Residential Construction print, housing starts soared +3.9% in July compared to the previous month and recorded a +5.9% increase from last year. But the results for building permits and completions are not as rosy. Permits declined by -13% compared to last year and completions dropped -11.8%, month-on-month and -5.4%, year-on-year. And then there’s August, where U.S. home builder confidence got too hot decided to take a dip – for the first time this year. The Housing Market Index, brought to you by the National Association of Home Builders/Wells Fargo, dropped 6 points from July’s peak and gave us a 50 on the confidence scale. It’s like the homebuilding sector suddenly decided to trade its double espresso for herbal tea.

If your project needs a caffeine boost, swing by; our espresso machine transforms coffee beans into pure liquid motivation, and we’d love to tell you all about Project Rescue.

STEEL and others

Gravity-defying drops in metal markets. It seems like hot-rolled coil (HRC) futures market is experimenting with keto and intermittent fasting because it shed 21.2% in the past 3 months. HRC prices are now back at levels last seen in January, trading below $730 per short ton (st)! The prices of ferrous construction materials are sliding with no exit ramp in sight. In July, PPI for steel mill products shrunk -7.6% from the previous month and -20.9% from last year. Switching our focus to cold-rolled steel sheet and strip, we see a jaw-dropping 24.1% plummet in PPI from the previous year, followed by -22% in steel pipe and tube.

But hold onto your hard hats and get ready to dig a little deeper into your pockets when renting or buying equipment. PPI for construction machinery and equipment is up +9.3% from last year. Elevators, escalators, and lifts are +6% more expensive and heating equipment warmed up by +5.9%. And that’s not the only show in town. Expect to pay more for nonmetallic mineral products. Cement +12.6%, concrete pipe +13.5%, ready-mix concrete +10.4%, flat glass +6.9%, year-on-year. But do you know what may cost you less? A CM that manages project risk like a hawk and delivers on cost saving strategies. Ask us how we do it.

See below for a commodities snapshot, or click here for the full report.